How a Reverse Mortgage May Help You Keep Your Home After Divorce in California

Strategies for Buying Out a Former Spouse, Keeping Your Home, or Purchasing a New Home Using a Reverse Mortgage

Written by John Correll, CRMP

Certified Reverse Mortgage Professional (CRMP)

Reverse Mortgage Specialist | 25+ Years of Mortgage Experience

Divorce Later in Life Can Create Difficult Financial Decisions

Divorce is never easy. When it happens later in life, it can change your retirement plans, your finances, and where you will live. One of the biggest challenges is that one home often becomes two, and the same money now has to support two households instead of one.

For many California homeowners, the family home is their biggest asset. Deciding whether to keep your home, sell it, or buy a new one can be one of the biggest financial decisions you’ll make. Many people think they only have two choices, but you may have more options than you realize.

A reverse mortgage may be one option worth exploring for some homeowners. This guide explains how a reverse mortgage may help in some California divorce settlements and what you should know before making an important financial decision.

✅ Key Takeaways

In this guide, you’ll learn how a reverse mortgage may help eligible California homeowners:

✓ Keep their home after divorce instead of selling it.

✓ Buy out a former spouse, eliminate the required monthly principal and interest payment, or purchase another home after divorce.

✓ Understand how Proposition 13 and Proposition 19 may affect housing decisions.

✓ Make informed housing and financing decisions that support retirement goals and long-term financial security.

Whether you’re buying out a former spouse, refinancing, or purchasing a new home, John Correll, CRMP can help you understand your reverse mortgage options. Call (619) 294-9820 or (888) 603-1550.

Why Divorce Can Be More Challenging for Older California Homeowners

Divorce later in life can bring different financial challenges than divorce at a younger age. There may be less time to rebuild your retirement savings, and the decisions you make now can affect your finances for many years.

Many older California homeowners have owned their homes for a long time. They may have built a large amount of home equity and may also have lower property taxes. Before deciding whether to keep your home, sell it, or buy a new one, it’s important to understand all of your options.

What Are Your Housing Options After Divorce?

One of the first questions many people ask is, “What should I do with the house?” The answer depends on your finances, your retirement plans, and your personal goals.

Four Housing Options When Getting Divorced

- Sell the home and divide the money.

- One spouse keeps the home.

- Buy a new home.

- Explore financing options, including a reverse mortgage.

There is no right or wrong answer. The best choice depends on your situation. The next sections explain each option in more detail.

Why Refinancing Can Be More Difficult After Divorce and During Retirement

Many people think they can simply refinance their mortgage after a divorce. While that may work for some homeowners, it can be more difficult if you’re retired or close to retirement.

After a divorce, you may be living on one income instead of two. Even if you have a lot of home equity, you may not qualify for a traditional mortgage. Or, you may qualify but not want another large monthly mortgage payment during retirement.

That’s why some homeowners start looking at other options. A reverse mortgage may be one option worth exploring.

Could a Reverse Mortgage Help During a Divorce?

If refinancing isn’t the right fit, a reverse mortgage may be another option to consider. In some California divorce cases, it may help one spouse keep the home, buy out a former spouse, or purchase a new home.

A reverse mortgage isn’t the right choice for everyone. But for some older homeowners, it may be one way to help settle the housing issues in a divorce and move forward with confidence.

Strategy #1: Buy Out a Former Spouse Using a Reverse Mortgage

Many people think they have to sell the family home during a divorce. In some cases, that may not be necessary.

A reverse mortgage may help one spouse buy out the other spouse’s share of the home. It may also help pay off an existing mortgage, making it easier for one spouse to stay in the home after the divorce.

How This Strategy May Work in a Divorce

Every situation is unique, but here’s one example of how the process may work.

- One spouse keeps the home as part of the divorce settlement.

- That spouse becomes the sole owner of the home.

- They apply for a reverse mortgage if they qualify.

- The reverse mortgage may help pay off the existing mortgage and buy out the former spouse’s share of the home’s equity.

Every situation is unique. Talk with your attorney, financial advisor, and reverse mortgage specialist before making a decision.

John’s Professional Insight

Many homeowners are surprised to learn they may have more options than they realize. I’ve seen situations where a reverse mortgage helped one spouse keep the family home instead of selling it. While it isn’t the right solution for everyone, it’s an option many people don’t know exists.

Strategy #2: The Spouse Who Keeps the Home May Eliminate the Monthly Mortgage Payment Using a Reverse Mortgage

In many divorces, the spouse who keeps the home must remove the other spouse from the existing mortgage. That usually means getting a new loan.

If you’re retired or living on a fixed income, you may not want another monthly mortgage payment. Even if you qualify for a traditional refinance, it may not be the best fit.

A reverse mortgage may be another option. By refinancing into a reverse mortgage, the existing mortgage is paid off and the required monthly principal and interest payment is eliminated. The homeowner must still pay property taxes, homeowners insurance, and keep the home in good condition.

How This Strategy May Work in a Divorce

While every divorce is different, this example illustrates one possible approach.

- One spouse keeps the home.

- They refinance into a reverse mortgage if they qualify.

- The required monthly principal and interest payment is eliminated.

The homeowner must continue to pay property taxes, homeowners insurance, and maintain the home.

John’s Professional Insight

Many homeowners tell me they don’t want another monthly mortgage payment during retirement. In some situations, a reverse mortgage may provide a way to keep the home while improving monthly cash flow.

Strategy #3: Purchase a New Home Using a Reverse Mortgage After Divorce

Sometimes the best choice is to sell the family home and move on. After the home is sold, the home equity is divided as part of the divorce settlement. While you may receive a substantial amount of cash, it may not be enough to buy another home outright, especially in many parts of California.

Many people don’t want another monthly mortgage payment during retirement. At the same time, they may not want to use all of their divorce settlement to buy a home with cash. A Reverse Mortgage for Purchase may be another option. If you qualify, you may be able to use part of your divorce settlement as the down payment and use a reverse mortgage to help buy your next home. This may allow you to keep more of your retirement savings while reducing or eliminating the required monthly principal and interest payment

How This Works in a Divorce

The following example shows one possible way a reverse mortgage may fit into the divorce process.

- The family home is sold and the home equity is divided.

- You decide to buy another home.

- You use part of your divorce settlement as the down payment.

- You use a Reverse Mortgage for Purchase if you qualify.

- The required monthly principal and interest payment may be reduced or eliminated.

The homeowner must continue to pay property taxes, homeowners insurance, and maintain the home.

John’s Professional Insight

Many people think they have to buy their next home with cash after a divorce. I’ve helped homeowners use a Reverse Mortgage for Purchase to buy a home that better fits their needs while keeping more of their retirement savings available for the future.

Have reverse mortgage questions? Speak directly with John Correll, CRMP at (619) 294-9820 or (888) 603-1550 for personalized guidance.

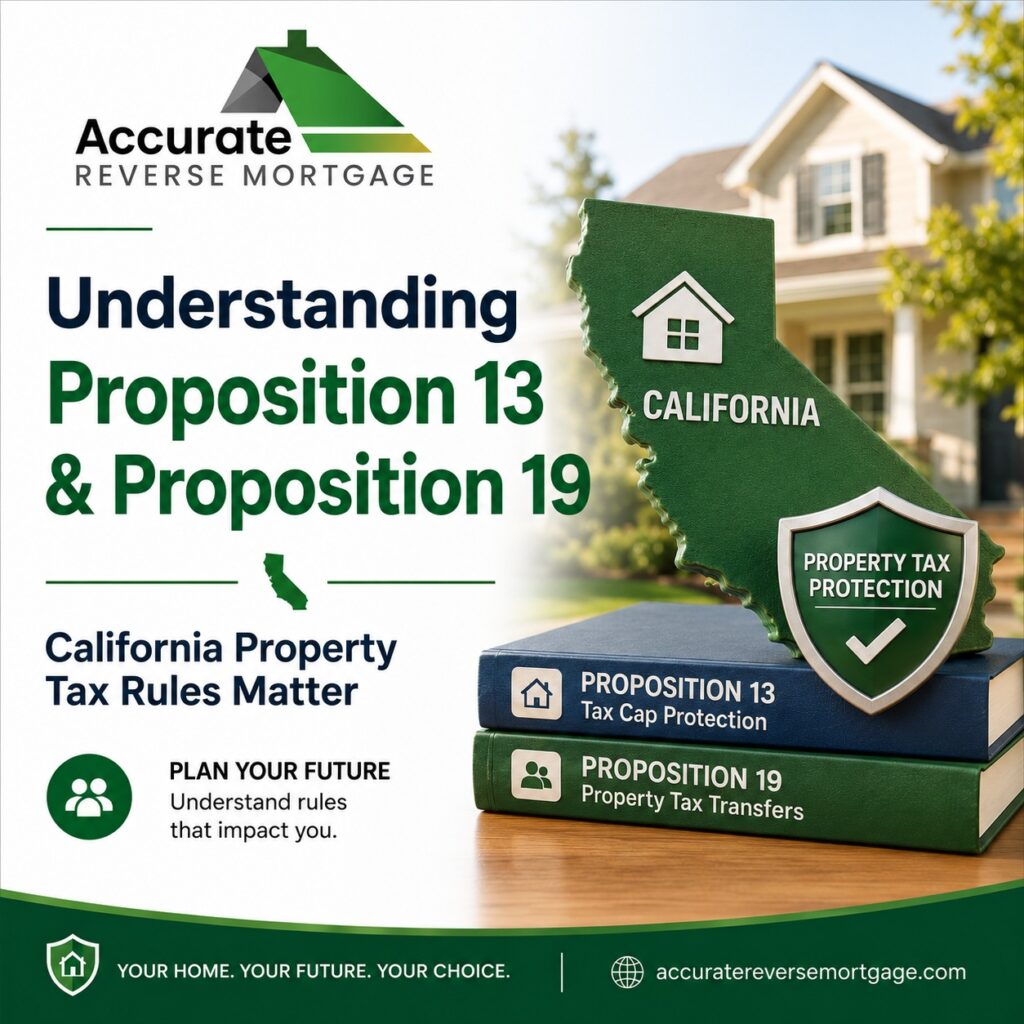

Preserving Your California Property Tax Base After Divorce

For many California homeowners, a low property tax base can be just as valuable as home equity. Before selling your home or buying another one after a divorce, it’s important to understand how your property taxes could change.

How Proposition 13 and Proposition 19 May Affect Reverse Mortgages After Divorce in California

In some situations, keeping your current home may help preserve your Proposition 13 property tax base. In other situations, Proposition 19 may allow eligible homeowners to transfer their property tax base to another home. If you’re considering a reverse mortgage after a divorce, understanding these California property tax rules may be an important part of your housing decision.

California Interspousal Transfer Deeds, the Divorce Exclusion, and Reverse Mortgages

When one spouse keeps the family home as part of a divorce settlement, an interspousal transfer deed may be used to transfer ownership. If the transfer qualifies for California’s interspousal transfer exclusion from property tax reassessment, the home may keep its existing Proposition 13 property tax base instead of being reassessed at its current market value.

If the spouse keeping the home later chooses a reverse mortgage, preserving the existing property tax base may be an important part of the overall financial strategy.

Important: This information is intended for general educational purposes only.

NOT TAX ADVICE: Property tax laws can be complex and may change over time. Every homeowner’s situation is different. Before making a final decision, talk with your attorney, tax advisor, and reverse mortgage specialist to understand how these California rules may apply to your situation.

Official California Property Tax Resources

California State Board of Equalization – Proposition 19 Resource Center

California State Board of Equalization – Property Taxes

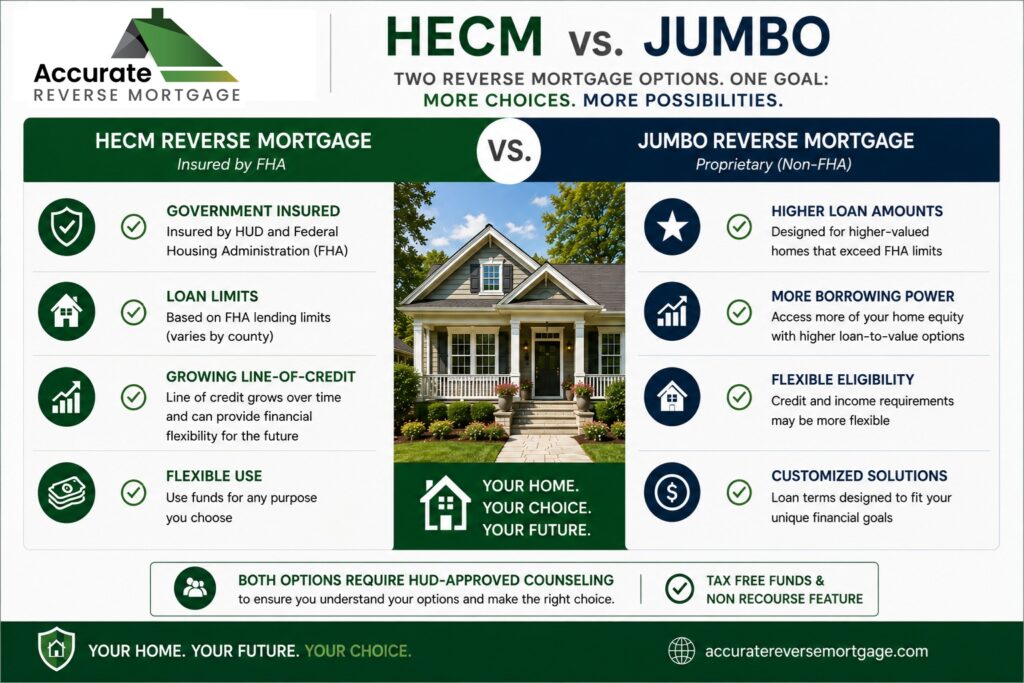

Types of Reverse Mortgages That May Help in a California Divorce: HECM vs. Jumbo

California’s higher home values often make it important to compare both an FHA-insured HECM reverse mortgage and a jumbo reverse mortgage. Depending on your home’s value and your divorce settlement, one option may be a better fit than the other.

The right choice depends on your home’s value, the equity in your home, and your financial goals after divorce. If you’d like to compare both options, I’m happy to explain the differences and help you decide which reverse mortgage may be right for you.

A Hypothetical California Divorce Example Using a Reverse Mortgage

Imagine a 70-year-old California homeowner who wants to keep her home after a divorce. She still has a mortgage, needs to remove her former spouse from the loan, and must pay him his share of the home’s equity.

Instead of selling the home or getting a traditional refinance, she explores refinancing into a reverse mortgage. If she qualifies, the reverse mortgage may allow her to remove her former spouse from the existing mortgage while helping her buy out his share of the home’s equity.

Every situation is unique. This example simply illustrates one way a reverse mortgage may help after divorce.

Questions to Ask Before Making a Housing Decision After Divorce

Before making a final decision, ask yourself these important questions:

- Do I really want to keep my home?

- Do I want another monthly mortgage payment during retirement?

- Can I comfortably afford my home over the long term?

- Should I sell my home and buy another one?

- How important is preserving my California property tax base?

- Have I compared all of my reverse mortgage options?

- Have I talked with my attorney, tax advisor, and reverse mortgage specialist?

If your answer is “No” to taking on another monthly mortgage payment, a reverse mortgage may be worth exploring.

Taking time to answer these questions may help you make a more confident decision.

Have questions?

Call John Correll, CRMP at (619) 294-9820 or (888) 603-1550 for a complimentary reverse mortgage consultation.

Frequently Asked Questions About California Divorce and Reverse Mortgages

Can a reverse mortgage help settle a divorce in California?

In some situations, yes. A reverse mortgage may help an eligible homeowner keep the family home, buy out a former spouse, or purchase another home after a divorce.

Can I Use a Reverse Mortgage to Avoid Selling My Home if I Get Divorced in California?

Possibly. If you qualify, a reverse mortgage may allow you to keep your home instead of selling it. Depending on your situation, it may also help you buy out your former spouse, refinance into a reverse mortgage, or eliminate the required monthly principal and interest payment.

Can I buy out my former spouse using a reverse mortgage?

Possibly. If you qualify and enough loan proceeds are available, a reverse mortgage may help you buy out your former spouse’s share of the home’s equity.

Can a reverse mortgage remove my former spouse from the current mortgage as part of a divorce?

In some situations, yes. If you qualify, refinancing into a reverse mortgage may replace the existing mortgage and help remove your former spouse from that loan as part of the divorce settlement.

When one spouse keeps the home, the deed transferring ownership may also be completed as part of the divorce settlement and the escrow process. Your attorney, escrow company, title company, and reverse mortgage specialist can work together to help coordinate the transaction.

Can the Reverse Mortgage Close at the Same Time as My Divorce Settlement?

In many situations, yes. A reverse mortgage may be coordinated with the divorce settlement and escrow process. This may allow the ownership transfer, loan closing, and other settlement terms to be completed at the same time.

The timing depends on the terms of the divorce settlement and the requirements of everyone involved, including the attorneys, escrow company, title company, and lender.

What Happens to My Existing Reverse Mortgage if I Get Divorced in California?

Getting divorced does not automatically make your reverse mortgage due and payable. If one spouse continues to live in the home and all loan requirements are met, the reverse mortgage may continue without any changes.

If the divorce settlement requires one spouse to be removed from the reverse mortgage, refinancing into a new reverse mortgage may be another option. This may allow the spouse keeping the home to remove the former spouse from the loan.

Can My Former Spouse Stay on an Existing Reverse Mortgage After Divorce?

It depends. If both spouses continue to live in the home and meet the loan requirements, there may be situations where the existing reverse mortgage can remain in place.

If the divorce settlement requires one spouse to leave the home or be removed from the reverse mortgage, refinancing into a new reverse mortgage may be another option.

Do I Have to Take on Another Monthly Mortgage Payment After a Divorce?

Not always. Depending on your situation, refinancing into a reverse mortgage may allow an eligible homeowner to eliminate the required monthly principal and interest payment. The homeowner must still pay property taxes, homeowners insurance, and maintain the home.

Can I Buy Another Home After Divorce Using a Reverse Mortgage?

Yes, if you qualify. A Reverse Mortgage for Purchase may allow you to use part of your divorce settlement as a down payment to buy another primary home.

Will I Still Own My Home?

Yes. You continue to own your home and remain on title. You must continue to pay property taxes, homeowners insurance, and maintain the home.

Does a Reverse Mortgage Affect Proposition 13 Property Taxes in California?

Generally, no. Simply getting a reverse mortgage does not, by itself, change your Proposition 13 property tax base.

However, property tax rules can be complex, especially after a divorce or when ownership changes. Talk with your attorney or tax advisor, and review the official California property tax resources included at the end of this guide to better understand how the rules may apply to your situation.

Is a Reverse Mortgage the Right Choice for My California Divorce?

Maybe. Every divorce is different, and a reverse mortgage is not the right solution for everyone. The best choice depends on your home, your finances, your retirement goals, and the terms of your divorce settlement. Understanding all of your options can help you make the decision that’s right for you.

Final Thoughts

Getting divorced does not always mean you have to sell your home. By understanding your housing and financing options, you can make a decision that supports your retirement goals and financial future.

If you’re going through a divorce and would like to explore whether a reverse mortgage may be an option, I’m happy to answer your questions and discuss your situation.

About the Author

John Correll, CRMP is a reverse mortgage specialist based in San Diego, serving homeowners throughout California. With more than 25 years of mortgage experience, John specializes exclusively in reverse mortgages and is dedicated to helping older homeowners make informed retirement decisions.

CRMP (Certified Reverse Mortgage Professional) is the highest professional designation in the reverse mortgage industry, recognizing experience, advanced education, ethical standards, and a commitment to serving older homeowners.

If you have questions about reverse mortgages and divorce, John is happy to help you explore your options.

Call or Text: (619) 294-9820

Toll Free: (888) 603-1550

John Correll, CRMP

Certified Reverse Mortgage Professional

NMLS #1004396, 2484031

CA Bur of Real Estate – Real Estate Broker #10353015, 02214678

John Correll, CRMP is a proud member of the National Reverse Mortgage Lenders Association (NRMLA), reflecting his commitment to professionalism, education, and helping homeowners make informed reverse mortgage decisions.

Resources for California Homeowners, Divorce, and Reverse Mortgages

The following official resources can help you learn more about reverse mortgages, California property taxes, divorce, and retirement planning.

Reverse Mortgage Resources

- U.S. Department of Housing and Urban Development (HUD) – Home Equity Conversion Mortgage (HECM) Information

- HUD-Approved HECM Counseling Agencies

- Federal Housing Administration (FHA) Reverse Mortgage Information

California Property Tax Resources

- California State Board of Equalization – Proposition 13 Information

- California State Board of Equalization – Proposition 19 Resource Center

- California State Board of Equalization – Property Tax Information

California Divorce Resources

Retirement Planning Resources

- Social Security Administration – Retirement Benefits

- Medicare.gov

- Internal Revenue Service (IRS) – Retirement Topics

Reverse Mortgage Counseling Resources

HUD-approved counseling is required before obtaining a federally insured HECM reverse mortgage. Counseling is provided by an independent HUD-approved counseling agency to help homeowners understand how the program works before making a final decision.

We are happy to provide a list of HUD-approved reverse mortgage counseling agencies in your area upon request. We also include a list of HUD-approved counseling agencies with every reverse mortgage proposal we prepare for our clients. If you have questions about the counseling process, we’re always happy to explain what to expect before you schedule your appointment.

Have Questions?

Every homeowner’s situation is unique. If you’d like to discuss your options or learn whether a reverse mortgage may be right for your situation, contact John Correll, CRMP.

(619) 294-9820

Toll-Free: (888) 603-1550

Complimentary reverse mortgage consultations are always available.